Taxi drivers across the US are starting to realize that they have lost the war against ridesharing companies and all their efforts to make regulations and lobby new laws were futile. They lost each battle and had lost the war.

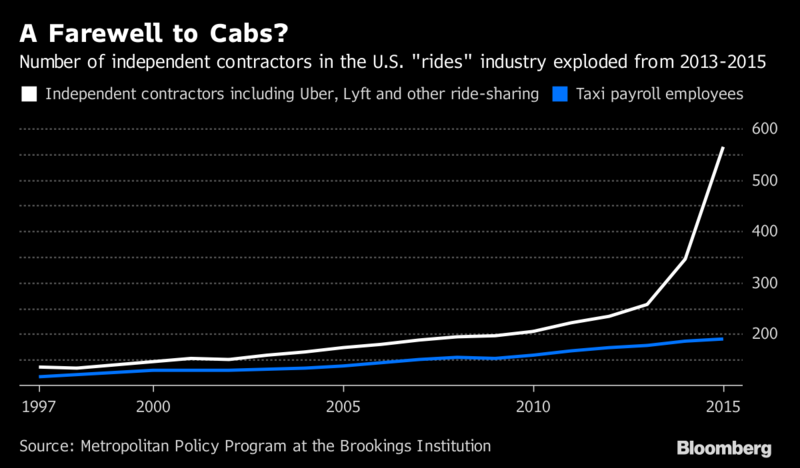

Brookings Institution analysis shows that the number of independent contractors in the rides sector grew by 174 percent in five years, compared with 21 percent only for cab company drivers: Photographer: Caitlin Ochs/Bloomberg

Cab companies and drivers are now re-branding themselves and joining ranks with the rideshare companies in direct competition on a local basis. For instance, Jamie Campolongo, President of what used to be Pittsburgh Yellow Cab, a company that has served Pittsburgh citizens for over a hundred years, is now called zTrip. This company offers a hybrid approach to Ubers strict credit card policy, by mixing in Taxi and ridesharing concepts in their app, zTrip now allows customers to either request a ride through the app or hail a car in the street. Passengers can pay with cash or credit card, and there are no surge or prime time price changes.

Campolongo didn't just stop by converting his taxi's into "cabshare," he allows independent contractors to join his ranks, the same way drivers join Uber and Lyft. Campolongo aptly stated that the pie is big enough for everyone to eat from.

The regulatory changes that Uber and Lyft invested millions of dollars in obtaining have made it easy for cab companies to come in line with the new regulations, such as background checks and commercial insurance, and also takes off the old streets cars since everyone is vying for a good comfortable and odorless ride.

Brookings institute performed an analysis that shows a phenomenal growth in rideshare drivers expanding by 174% in five years where the taxi industry only increased by 21% in the same time. Many cab companies went bankrupt, being unable to compete with Uber and Lyfts control of the market, while other companies adapted to the new situation.

zTrip is a classic example of adaptation, evolution in the face of extinction. This company was prepared for the last Steeler's home game, having 426 cars on the roads, 300 were cabs, and 126 were independent contractors. It was the first time they had so many cars out at one moment. The beauty of "cab sharing" is that you don't need to have a set number of cars online, the number varies based on saturation and need.

The TLPA (Taxicab, Limousine and Paratransit Association) has also changed direction, once it fought Uber and Lyft through campaigns such as "who's driving you?" and now under Michael Pinckard, their new head, they firmly understand that this is the new future of the human logistics industry. Pinckard stated that it was obvious, based on how the last year's statistics that ridesharing is now a standard feature of the transportation industry.

Uber was not the first to think the ridesharing idea up, neither Sidecar that put a patent out on the first app back in 2002. C&H Taxi's in Charleston, West Virginia asked way back in the 1980's for permission to allow their drivers to use private cars for Taxi services but then the laws were unchangeable, and it was illegal to do so.

When Uber came on the scene and started to bully their way into State, and the Federal legislature then too did Jeb Corey, owner of C&H start to adapt to the new situation.

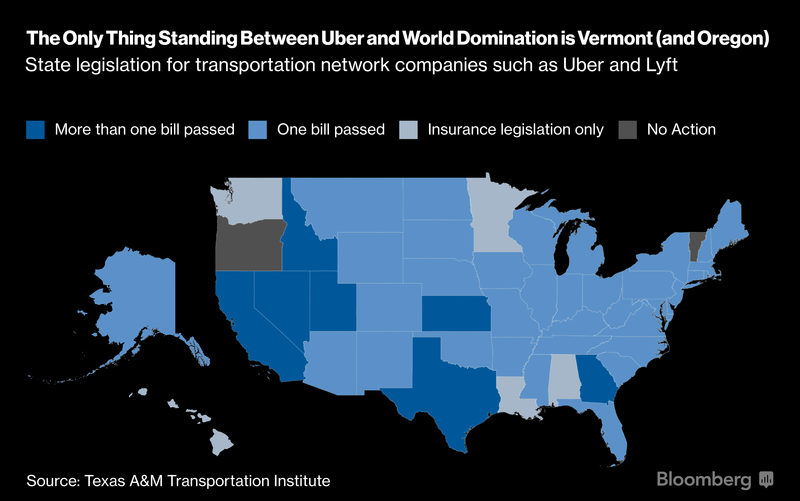

The state of California was the first to define and set regulations when in 2013 the Public Utilities Commission termed the "ridesharing" business as "Transportation Network Companies" or TNC's, which was a new term used to define them apart from Taxies and Limousine services.

Over the last four years, forty-three states and DC passed many new laws and regulations that cover everything including fees for background checks, background check standards and permits for drivers. Most of the other States used the CA TNC definition for their State regulations.

Apart from the 43 states and DC, another five states have regulated rideshare insurance issues, they are Louisiana, Alabama, Hawaii, Minnesota, and Washington, and only two states stand between ridesharing and complete US coverage, they are Oregon and Vermont.

Uber and Lyft spent around $14 million between 2012 and 2016 lobbying states; this amount is equal to over 75% of all the Taxi sectors national spend at the same time. Over the past four years, Uber and Lyft have changed the face of the industry, putting many taxi companies out of business but opening new avenues of income for many other adapting companies and newcomers.

Uber is still the countries leader, with over $70 billion valuation placed through private investment, the last investment amount due to come to a $10 billion injection of capital very soon from Softbank (Japan). Lyft has a value of $11 billion including the last-minute $1 billion from Alphabet that had abandoned Uber due to corporate espionage accusations. Uber and Lyft now cover most of the US and continue to hog the market nationally. Uber maintains a 56% market lead over Lyfts 11%, but since many taxi companies are either going out of business or adapting, the final figures are yet to become firm.

Uber and Lyfts regulation drive have made it easier for competitors to enter the market, now that the market has been frame worked for them. Cab companies around the US are using the TNC designation to restructure themselves, creating hybrid solutions that outperform Uber and Lyfts rigid solutions. Another issue is the parking zone issue; Taxi companies have specific standing zones as well as Airport status, this gives them an added advantage over ridesharing companies. These changes will blur the lines soon since Uber only now has San Francisco looking at ridesharing parking zones, once cab companies become full hybrids, the concept of a separate Taxi and Ridesharing zone will be eradicated. So, while one industry helped the other adapt and evolve, the first industry will eventually have to share its resources with the second, and the time will come when there will be only one designated human logistics solution.

This future looks even more real, when considering that Campolongo and Corey have asked state regulatory agencies to enable them to continue operating as normal cab companies with a central dispatch and street hails, they are asking to add TNC as a definition for allowing them to contract freelance drivers too.

The current State regulations are against the survival of Taxi's; the new TNC model will always enable ridesharing companies to out-compete them. Most taxi services agree that their future is bleak and need to consider how to change regulations to include the new hybrid status.

This new "if you cannot beat them, join them" concept works well for large cab companies but for most of the small ones and independent drivers, the costs and regulations are too steep for them, and they will be replaced by the rideshare and cabshare companies.

Now that the Federal and State lawmakers have realized that Uber and Lyft are here to stay, they are starting to create new regulations and laws that will continue to fluctuate and change as the new national status is being comprehended and cab companies start to adapt and evolve.

The biggest issue facing Uber and Lyft are hybrid companies that can undercut their pricing and service scheme. Both companies are still not profitable, and in fact so deep in losses; they operate out of private investor money. Uber is trying to reach an IPO before it goes under and the new Softbank deal will save it. Lyft is slowly progressing but has not yet reached profitability.

In fact, there is no real difference between cab companies and ridesharing, when you look at a cab company using a central dispatch, you are looking for a driver app in human form. The app is the central dispatch, the back office of support for customers and drivers are the extra overheads that Uber and Lyft have to pay while the machine shops are the overheads that taxi companies have to pay for maintaining their fleets. It's a financial model difference, where the old rules meant owning a fleet of cars and employing drivers but having no office support, or only employing office support and contracting drivers with their cars using strict requirements. In the case of Uber and Lyft, it's a matter of when will they become profitable? Where is the fine balance between income generated from app usage and service fees to investment in HR and R&D? With cab companies the proof is already there, they are profitable. Will the new hybrid service kill the uni-focused service? This is the main question being opened up now, and the final question is, how will autonomous cars affect the status quo?

Once you remove the driver from the equation what will the US do with millions of unemployed people whose only source of income was from driving a car? While the world is on a rampant research charge to kill an entire sector, human drivers, has anyone yet raised the question of how their states and nations will deal with the death of a major source of income for a large percentage of their population. Autonomous cars don't stop with ridesharing; they will go onto replacing bus, truck and shuttle drivers. Perhaps the only safe sector is the parcel and food delivery sector, but I am sure that some genius will come up with an app to kill that source of income too.